PART A: Operations and Affairs of the Bank

ORGANISATIONAL STRUCTURE OF THE BANK OF NAMIBIA

MEMBERS OF THE BOARD

Click here to view the Members of the Board (31 December 2023)

THE BANK'S SENIOR MANAGMENT

Click here to view the Bank’s Senior Management Team as at 31 Match 2023

MANAGEMENT STRUCTURE

Click here to view the Management structure as at December 2023

GOVERNANCE

OBJECTIVES AND ACCOUNTABILITY OF THE BANK

Click here to read more about the Objectives and accountablity of the bank

CORPORATE CHARTER

Click here to access the Corporate Charter

STRATEGIC PLAN 2022–2024

The Bank’s Strategic Plan is linked to its mission and functional priorities.

Following the launch of the Bank’s three-year Strategic Plan on 1 December 2021, the focus for the Bank has been on executing the Strategic Plan, with 2023 being no exception. The Bank stayed true to the Strategic Plan, which continued to set the direction and clear priorities to align departments towards a common goal which, in turn, clarifies and simplifies decision-making. Through the three-year strategy, the Bank aims to recalibrate, repurpose, reprioritise and become future-fit. To achieve this, it is envisaged that the Bank will become a digitally transformed institution with a fully modernised financial system that can help restore economic growth and sustain economic development. In 2023, the Bank conducted biannual strategy reviews in May and November. These sessions involved cumulative reviews that evaluated not only the progress made within the year, but also the overall progress towards successfully completing the three-year Strategic Plan in 2024. Simultaneously, careful consideration was given to prioritising key initiatives for the attainment of this goal.

ACCOUNTABILITY

The Bank is committed to good corporate governance practices and accountability to the public.

It is of paramount importance that the Bank always remains accountable to the public at large by adhering to sound corporate governance principles. Relevant legislation and the Bank’s Corporate Charter and Strategic Plan are amongst the tools that guide the Bank in living up to the standards of good governance. The Bank also strives to be transparent by its concrete communication strategy that enables open and clear expression of why and how the Bank acts as it does. The aspects of good governance that the Bank is committed to meet include:

- being responsible, respected, trustworthy, and credible;

- being accountable to its shareholder – the Government – and the Namibian people;

- demonstrating an exceptionally high degree of integrity;

- ensuring that its actions and policies are efficient, effective and transparent;

- maintaining professionalism and excellence in the delivery of its services; and

- being flexible and forward-looking in its approach, while still avoiding undue risk.

THE GOVERNOR

The Governor serves the Bank as its Chief Executive Officer (CEO) and is accountable to the Board for the management of the Bank and the implementation of its policies.

The Governor also represents the Bank in its relations with the Government and other institutions. In most other matters, comprehensive and Board-approved delegations of authority are in place to enable the Governor and his delegates to carry out their duties related to the implementation of policies. Ordinarily, the Governor is appointed for a five-year term. The Act sets specific criteria for the appointment, reappointment, and dismissal of a Governor. The current incumbent, Mr. Johannes !Gawaxab, was reappointed for a five-year term, effective from 1 January 2022 to 31 December 2026.

THE BOARD OF THE BANK OF NAMIBIA

The Board is responsible for the policies, internal controls, risk management and general administration of the Bank.

In addition to their typical fiduciary duties, Board members are also charged with many high-level responsibilities directly related to the policies and operations of the Bank, including approving the licensing of banking institutions and ensuring the prudent management of international reserves. In addition, the Board is responsible for approving the Bank’s financial statements and annual budget, promoting effective corporate governance practices, and monitoring internal controls and risk management frameworks.

The Bank’s Board members are appointed by the President of the Republic of Namibia.

They consist of the Chairperson (executive member), two further executive members, one ex officio member (non-executive), and a minimum of five and a maximum of six further non-executive members. The Governor (Chairperson) and the Deputy Governors are the executive members, while the Executive Director of the MFPE is the ex officio member. In addition, not fewer than five but not more than six non-executive members of the Board are appointed with due cognisance of their respective skills and areas of expertise in the fields of central banking, economics, the banking sector, finance, law, business, commerce and such other disciplines as may be relevant to the execution of the Bank’s mandate.

The Board meets regularly (at least four times a year) with the main purpose of overseeing and monitoring the Bank’s finances, operations and policies.

During 2023, four ordinary and two special Board meetings were held. Table A.1 below sets out the dates of Board meetings and the attendance of members during 2023:

/Board-Attendance.png.aspx?lang=en-ZA)

The Board delegates certain functions to its sub-committees (the Information Technology Governance and Projects Committee (ITGPC), the Audit Committee, and the Remuneration Committee).

All these sub-committees are important elements of the Bank’s sound corporate governance structure, have been established through formal terms of reference, and report to the Board. The Board can assure stakeholders that the sub-committees held regular meetings during the period under review and that they met their respective obligations in all material respects.

The ITGPC was established to assist the Board in discharging IT-related duties and responsibilities.

The purpose of the Committee is to perform a strategic oversight role to ensure alignment of the IT strategy with the Bank’s strategy through the approval, prioritisation and monitoring of strategic IT projects and initiatives for value creation, risk mitigation and resource allocation. The ITGPC is comprised of three non-executive Board members, and its meetings are held quarterly. The dates of the ITGPC meetings and the attendance of members during 2023 are outlined in Table A.2.

/ITGPC-Attendance.png.aspx?lang=en-ZA)

The Audit Committee is responsible for evaluating the adequacy and efficiency of the Bank’s corporate governance practices, including its internal control systems, risk control measures, accounting standards, and auditing processes.

Three independent non-executive Board members currently serve as members of the Audit Committee, whose meetings are also attended by the Bank’s Deputy Governors; Director: Finance and Administration; Head of Risk Management and Assurance; the external auditors; and relevant staff members. In general, the Audit Committee is responsible for considering all audit plans and the scope of external and internal audits to ensure that the coordination of audit efforts is optimised.

The Audit Committee is also required to introduce measures to enhance the credibility and objectivity of financial statements and reports prepared regarding the affairs of the Bank, and to enhance the Bank’s corporate governance, with emphasis on the principles of accountability and transparency. Table A.3 below summarises the dates of the Audit Committee meetings and the attendance of the audit committee members during 2023.

/Audit-Attendance.png.aspx?lang=en-ZA)

The Remuneration Committee is responsible for overseeing and coordinating the Bank’s remuneration policy and strategy to ensure its competitiveness and comprehensiveness, in order to attract and retain quality staff and Board members.

/Remuneration-Attendance.png.aspx?lang=en-ZA)

This Committee consists of three non-executive Board members and the Deputy Governor designated to this area. The dates of the Remuneration Committee meetings and the attendance of members during 2023 are set out in Table A.4.

MANAGEMENT STRUCTURE

The Bank’s Senior Management Team as at the end of 2023 consisted of the Governor, two Deputy Governors, and the Directors of the Bank’s various departments.

To ensure that the Bank implements its policies effectively, several committees are in place. These are the Monetary Policy Committee (MPC); the Financial System Stability Committee; the Macroprudential Oversight Committee (MOC); the Management Committee; the Investment Committee; the Risk Management Committee; the Digital Transformation Management Committee; the Budget Committee; and the Tender Committee.

The function of the MPC is to implement an appropriate monetary policy stance. The MPC in 2023 was comprised of the Governor (Chairperson); the two Deputy Governors; the Director: Research and Financial Sector Development Department; the Director: Financial Markets Department; the Technical Advisor to the Governor; the Advisor on Monetary and Economic Matters; and the Director: Strategic Communications and International Relations. The MPC normally meets every second month to deliberate on an appropriate monetary policy stance to be implemented by the Bank in the subsequent two-month period. All decisions relating to monetary policy matters are taken by consensus. In seeking consensus, each member expresses his or her view regarding the appropriate policy stance, with motivation. Where consensus does not emerge, the Chairperson may exercise his/her casting vote. The view of each member is recorded along with the member’s reason(s) for holding such a view. The monetary policy decision is communicated to the public through a media statement delivered at a media conference.

The Financial System Stability Committee assesses the vulnerability and risk exposure of the entire financial system. It is an inter-agency body set up between the Bank and the Namibia Financial Institutions Supervisory Authority (NAMFISA), with the MFPE as an observer.

The Management Committee is responsible for reviewing the Bank’s policies on financial and other administrative matters. The Management Committee is comprised of the Governor (Chairperson); the Deputy Governors; the Advisor(s) to the Governor; all Directors; and the Head of Risk Management and Assurance. The Management Committee meets every second week.

The Investment Committee is responsible for reviewing the management of Namibia’s foreign exchange reserves. While the Board approves the International Reserves Management Policy, the Investment Committee reviews the investment guidelines for final approval by the Governor. The Investment Committee is also expected to ensure that investments comply with the approved policy. The Investment Committee is comprised of the Governor (Chairperson); the Deputy Governors; Advisor(s) to the Governor; the Director of the Financial Markets Department; the Director of the Research and Financial Sector Development Department; the Director of the Strategic Communications and International Relations Department; and the Director of the Finance and Administration Department.

The Risk Management Committee assists the Audit Committee to ensure that the Bank implements an effective risk management policy. The Committee also supports the annual strategic focus areas, thereby enhancing the Bank’s ability to achieve its Strategic Objectives and ensure that disclosure regarding risks is comprehensive, timely and relevant. The Committee is comprised of all members of the Management Committee and is chaired by the Governor or a Deputy Governor. Its meetings are held on a quarterly basis, preceding the Audit Committee meetings.

The function of the Budget Committee is to oversee the budget deliberations of the Bank. The Budget Committee meets as part of the normal annual budget process of determining and providing for the Bank’s income and expenditures (both operational and capital) to be incurred in the execution of its functions and responsibilities. Each department presents and defends anticipated annual budgetary allocations before the Budget Committee. The Budget Committee members are the Governor (Chairperson); the Deputy Governors; and the Director and senior staff members of the Finance and Administration Department, which also provides administrative and support services. One representative each from the Employee Liaison Forum (ELF) and the employees’ bargaining union are permitted to attend and participate in the budget deliberations to ensure transparency.

The Tender Committee is responsible for ensuring sustainable, ethical, transparent, and cost-effective procurement of and tendering for the Bank’s assets, goods and services. To achieve these objectives, the Committee takes into consideration the following:

- quality of the product/service;

- cost/price;

- reliability of suppliers;

- delivery time and after-sales service support; and

- support to Small and Medium-sized Enterprises (SMEs)

The key objectives of the Digital Transformation Management Committee are to determine and align the Strategic Objectives of the Bank with cross-departmental matters of Digital Transformation, Technology, Projects, Processes and Overall Efficiency within the Bank. The DTMC members are the Governor (Chairperson); Deputy Governors; Advisor(s) to the Governor; and all departmental heads. The Head: Risk Management and Assurance, the Deputy Director: Strategy, Projects and Transformation, and the Director: Information Technology are permanent attendees who serve in the capacity of Advisors to the Committee. The DTMC meets at least four times per calendar year.

REPORTING OBLIGATIONS

The 2020 Bank of Namibia Act requires the Bank to submit various reports to the Minister of Finance. The requirement includes the obligation to submit a copy of the Bank’s Annual Report to the Minister of Finance within three months after the end of each financial year. The Minister, in turn, is required to table the Annual Report in the National Assembly within 30 days of receiving it. The Report must contain the Bank’s annual accounts, certified by external auditors, information about the Bank’s operations and affairs, and information about the state of the economy. Apart from the Annual Report, the Bank is further required to submit a monthly balance sheet, which is published in the Government Gazette.

THE YEAR UNDER REVIEW

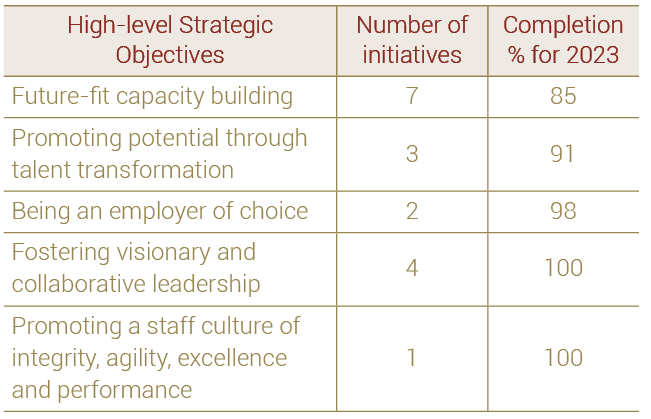

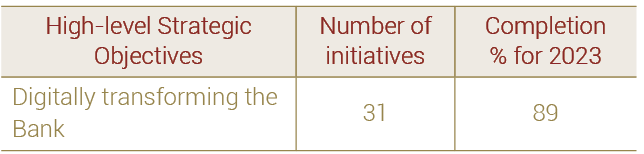

The Bank has four main strategic focus areas, namely: the Purpose Pillar, the Stakeholder Engagement Pillar, the Talent and Transformation Pillar, and the Future-fit Organisational Efficiency and Effectiveness Pillar with Digital Transformation serves as the Key Enabler. Each of these pillars consists of High-level Strategic Objectives that the Bank aspires to achieve. These Strategic Objectives are directly connected to the Bank’s functional priorities, its Mission, its Vision, and developments in the internal and external environments. Below is an overview of the Bank’s Strategic Pillars and their corresponding High-level Strategic Objectives.

In order to ensure successful implementation of the Strategic Plan, the Strategic Objectives have been divided into strategic initiatives, with clear and measurable targets. In 2023, the Bank conducted biannual strategy reviews in May and November. These sessions involved cumulative reviews that evaluated the overall advancement towards completing the three-year strategic plan. By the end of 2023, the Bank had made noteworthy progress, completing 68% of the comprehensive three-year plan and meeting 93% of the specific goals set for 2023. The substantial progress made can be credited not just to the clear goals aligned with the Strategic Plan’s objectives, but also to the explicit definition of strategic outcomes. This was evident in the unwavering commitment of each department to the Bank’s strategy and its intended impact.

In this section, the High-Level Strategic Objectives are presented in a tabular format with performance measures expressed in terms of the completion rate percentage. These performance outcomes are complemented and further substantiated by a summary of key actual outcomes and achievements during the year. The more detailed discussions on specific Strategic Objectives initiatives follow in this Section.

Purpose Pillar

|

Stakeholder Engagement Pillar

|

Talent and Transformation Pillar

Key Enabler: Digital Transformation

|

Future Fit Pillar

|

FINANCIAL STABILITY ASSESSMENT AND SURVEILLANCE

The Bank assesses risks and vulnerabilities that could threaten financial sector stability to determine the sector’s resilience and ability to withstand internal and external shocks. These risks are assessed in the Financial Stability report, which is published in April each year and is followed by an internal review in September. Risks to financial stability in Namibia have been and will continue to be monitored accordingly under the advisory guidance of the Financial System Stability Committee and the direction of the Macroprudential Oversight Committee (MOC). All high-level strategic initiatives pertaining to the assessment of risks and vulnerabilities in the financial system were completed in 2023. Furthermore, the Bank has been given enhanced resolution powers under the Banking Institutions Act (No. 13 of 2023). The Bank’s powers enable it to mitigate the risks posed by the failure of a banking institution.

Namibia’s financial system remained stable given the current macroeconomic environment. During 2023, the domestic financial system remained stable, robust, and resilient, withstanding elevated risks and vulnerabilities emanating from the global and domestic economic and financial environments. Both the banking and non-banking financial sectors continued to perform adequately and remained resilient during 2023. Moreover, the banking sector remained liquid and well capitalised, while the non-banking financial industry reported funding and solvency positions above the prudential limits.

The Banking sector and non-banking financial institutions (NBFIs) continued to be profitable, liquid, and well capitalised. Both the capital adequacy and the liquidity position of the banking sector improved and remained above the statutory minimum requirements. Profitability increased during 2023, reaching pre-pandemic levels, as observed in both the return on assets and return on equity. Asset quality, as measured by the non-performing loans (NPLs) ratio, remained stable and below the crisis time supervisory intervention trigger point of 6.0 percent, at the end of 2023. The NBFI sector withstood the headwinds of the macroeconomic environment, characterized by slowing growth in the domestic economy; volatility in global financial markets; elevated inflation rates; and correspondingly, high interest rates. The demand for NBFI products was observed to remain sound in 2023, while investment assets performed positively. Overall, the banking sector and NBFIs reported sound developments with adequate containment of threats to financial system stability.

During the review period, the Bank continued to support the Namibia Deposit Guarantee Authority. The Namibia Deposit Guarantee Authority is mandated to manage the Deposit Guarantee Scheme, the purpose of which is to protect depositors in the event of bank failures. This is done by ensuring that deposits are reimbursed in an efficient, transparent, and speedy manner. The Scheme is considered a necessity in the financial sector as its existence provides confidence in the system and reduces the risk of a financial system crisis.

PAYMENT SYSTEM OVERSIGHT

The Bank continued to fulfil its regulatory mandate as the overseer of the National Payment System (NPS) in 2023, in line with the Payment System Management Act (No. 14 of 2023). Payment systems are a crucial part of the financial infrastructure of a country. In Namibia, the regulatory mandate to oversee the NPS was accomplished through risk-based on-site and off-site oversight activities. The Bank conducted off-site activities by monitoring system participants through a combination of assessments based on information provided by the regulated institutions in the NPS. During the review period, the Bank conducted five risk-based inspections of various participants. The observations from the assessments have been shared with the respective participants to be addressed within the agreed timelines.

Following the introduction of the Payment System Management Act during the year under review, the Bank commenced with revising its regulatory framework to ensure the alignment of regulations (Determinations, Directives, etc.) with the new Act. The new Act empowers the Bank to be the sole regulator of the NPS, thus withdrawing the powers previously vested in the Payments Association of Namibia (PAN) to license and oversee payment service providers. In terms of the Act, PAN will continue to operate as an advisory and collaborative body for setting technical rules and standards for its members to participate in the NPS.

The Act established the collective term ‘payment service providers’ in reference to both banking institutions and non-bank financial institutions authorised and licensed to offer payments services, as listed in the Schedule of the Act. In line with this stipulation, the Bank revised the current Determination on Issuing of a Payment Instrument (PSD-1) to provide requirements for the licencing and authorisation of payment service providers in Namibia. The revised PSD-1, the Determination on the Licensing and Authorisation of Payment Service Providers in Namibia also includes specific requirements for the various payment service provider categories and repeals various instruments previously used to license and oversee payment service providers in the NPS.The revised PSD-1 was gazetted on 15 February 2024.

Furthermore, during the review period, the Bank undertook a comprehensive review of the Determination on Issuing Electronic Money in Namibia (PSD-3), set to be gazetted in the first quarter of 2024. Similarly, this revision intends to align PSD-3 with the Payment System Management Act (No.14 of 2023) and the National Payment System Vision and Strategy (2021–2025). The proposed revised PSD-3 aims, among other objectives, to provide a level playing field for e-money issuers to enhance financial inclusion, promote competition, accommodate interoperable wallets, encourage the development of innovative products and services, enhance the capabilities of wallets, and align with international best practises in the e-money ecosystem.

PAN established an Open Banking Forum during the period under review. Open Banking allows third-party and other financial service providers to access customer data at banking institutions to provide customers with other value-added financial services not offered by banking institutions. The Forum comprises representatives from various institutions, namely banking institutions, non-bank financial institutions, the PAN Stakeholder Forum, the Bank of Namibia, and NAMFISA (the Namibia Financial Institutions Supervisory Authority). The Forum enables the various stakeholders to discuss issues of mutual interest pertaining to the adoption of Open Banking and to facilitate consultations on the Bank’s Open Banking Position Paper. The Bank intends to issue an Open Banking regulation in 2024 to operationalise the modernisation of the payment system, broaden service offerings, and improve customer convenience, amongst others.

SETTLEMENT SYSTEM

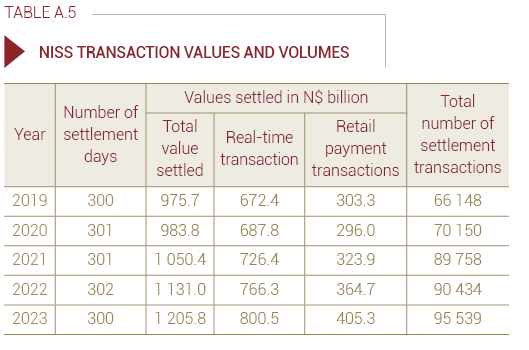

In 2023, the Bank provided interbank settlement services through the NISS to authorised institutions. The interbank transactions settled through the NISS comprise single-item time-critical transactions processed by the participants in the NISS, and retail payments such as electronic funds transfers (EFTs) and card transactions, that are cleared through Namclear. During 2023, the Bank conducted one announced NISS disaster recovery exercise during the first quarter of the year. The disaster recovery exercise was unsuccessful as the two-hour recovery time objective was not met due to IT-related issues. The Bank engaged in work to resolve these issues, which resulted in the success of the subsequent unannounced NISS disaster recovery exercise, conducted during the third quarter of 2023. Additionally, no business continuity management exercise was performed during 2023 due to IT infrastructure upgrades.

During 2023, the Bank recorded a slight increase in settlement volume and value. The aggregate settlement value recorded in the NISS during 2023 was N$1 205.8 billion, with a volume of 95 539 transactions, which translates to an average of 319 transactions per settlement day. The total value and volume settled through the NISS between 2022 and 2023 increased by 6.6 percent and 5.7 percent, respectively. Moreover, the share of single transactions settled in the NISS amounted to N$800.5 billion, which translates to 66.4 percent of the total value settled. The value of retail payment transactions cleared through Namclear was N$405.3 billion, which represents 33.6 percent of the aggregate value settled.

CLEARING SYSTEM

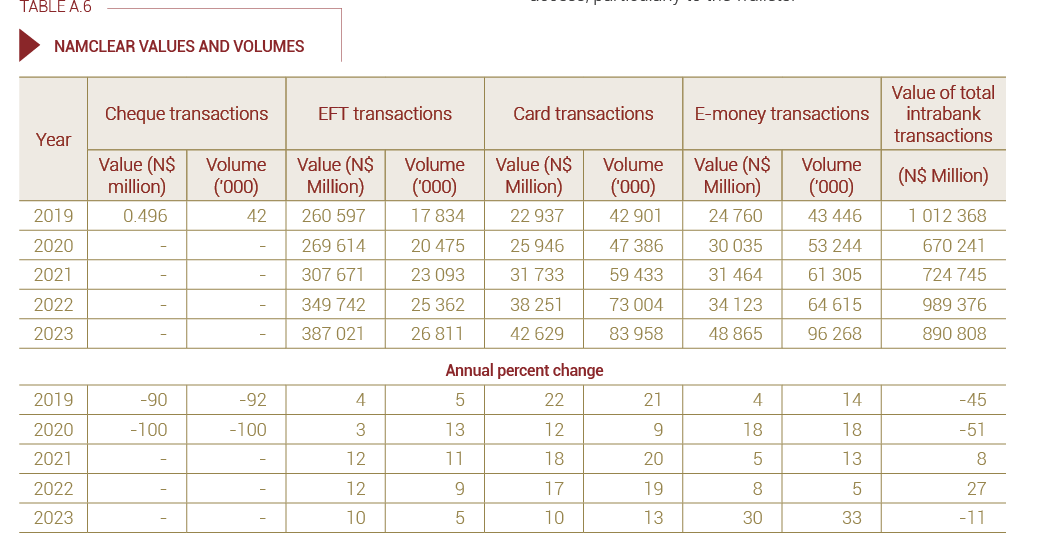

The Bank continued to oversee clearing operations in the NPS. During the review period, Namclear was the only payment service provider that provided clearing services within the NPS. It clears interbank EFT and card transactions, which are submitted to the NISS for settlement.

The value of EFT transactions processed by Namclear was significantly higher in 2023 than in 2022. EFT transactions processed increased to 27 million, valued at N$388 billion, which represents a 9 percent increase in volume and a 10 percent increase in value. The increase in EFT usage could be attributable to increased economic activity.

Card payment transactions continue to increase year-on-year. In 2022, Namclear processed card transactions with a total value of N$38.2 billion. The value and volume processed by Namclear increased by 17 percent and 19 percent, respectively, over the 2021 figures.

INTRABANK AND ELECTRONIC-MONEY SCHEMES

The value of EFT intrabank transactions decreased in 2023. The EFT intrabank transactions processed in 2023 amounted to 47 million, valued at N$834 billion, down from the N$922.7 billion reported in 2022. The decrease in EFT usage can be attributed to the use of electronic money (E-money), which is the payment stream most preferred by consumers.

Payment card intrabank transactions in 2023 increased over the transactions reported in 2022.Card transactions processed between merchants and customers of the same banking institution amounted to 766 million, valued at N$57 billion, which is a moderate decrease from the N$66 billion reported in 2022.

The use of E-money schemes, which are currently close-loop (i.e., only operating within the same banking institution’s systems) continued to increase in 2023. The Bank observed a significant increase in the use of E-money as a payment instrument, which shows a shift in the payments behaviour of consumers of the domestic payment system. In 2023, the value and volume of E-money increased to N$49 billion and 96 million, respectively. This increase can be attributed to consumer behaviour changing as a result of ease of use and access, particularly to the wallets.